Autonomous Driving Market Opportunities: Where the Real Value Lies Through 2031

The global Autonomous Driving Market Opportunities through 2031 are as varied, as geographically distributed, and as commercially consequential as those in any technology market of the current era. According to The Insight Partners, in a market growing at 16.3% CAGR, the most compelling opportunities are concentrated in four categories that each offer genuine competitive positioning advantages for companies willing to engage with the specific technical and commercial requirements of autonomous driving applications. The first is the emerging market geographic expansion opportunity, where rapid industrialization and infrastructure investment in Asia-Pacific and Latin America are creating new demand for autonomous vehicle systems and connected mobility solutions.

The second is the AI software platform opportunity, where the shift from hardware-defined to software-defined vehicles is creating recurring revenue models that are more financially attractive than one-time hardware sales economics. The third is the safety and regulatory compliance opportunity, where tightening safety mandates are creating compliance-driven demand for ADAS features that function as the stepping stone to higher automation levels. The fourth is the Mobility-as-a-Service integration opportunity, where autonomous driving technology is enabling entirely new commercial models for transportation service delivery that have no viable conventional vehicle equivalent.

Get exclusive insights into the Autonomous Driving Market – https://www.theinsightpartners.com/sample/TIPRE00007953

What Is Autonomous Driving and Where Are the Opportunities?

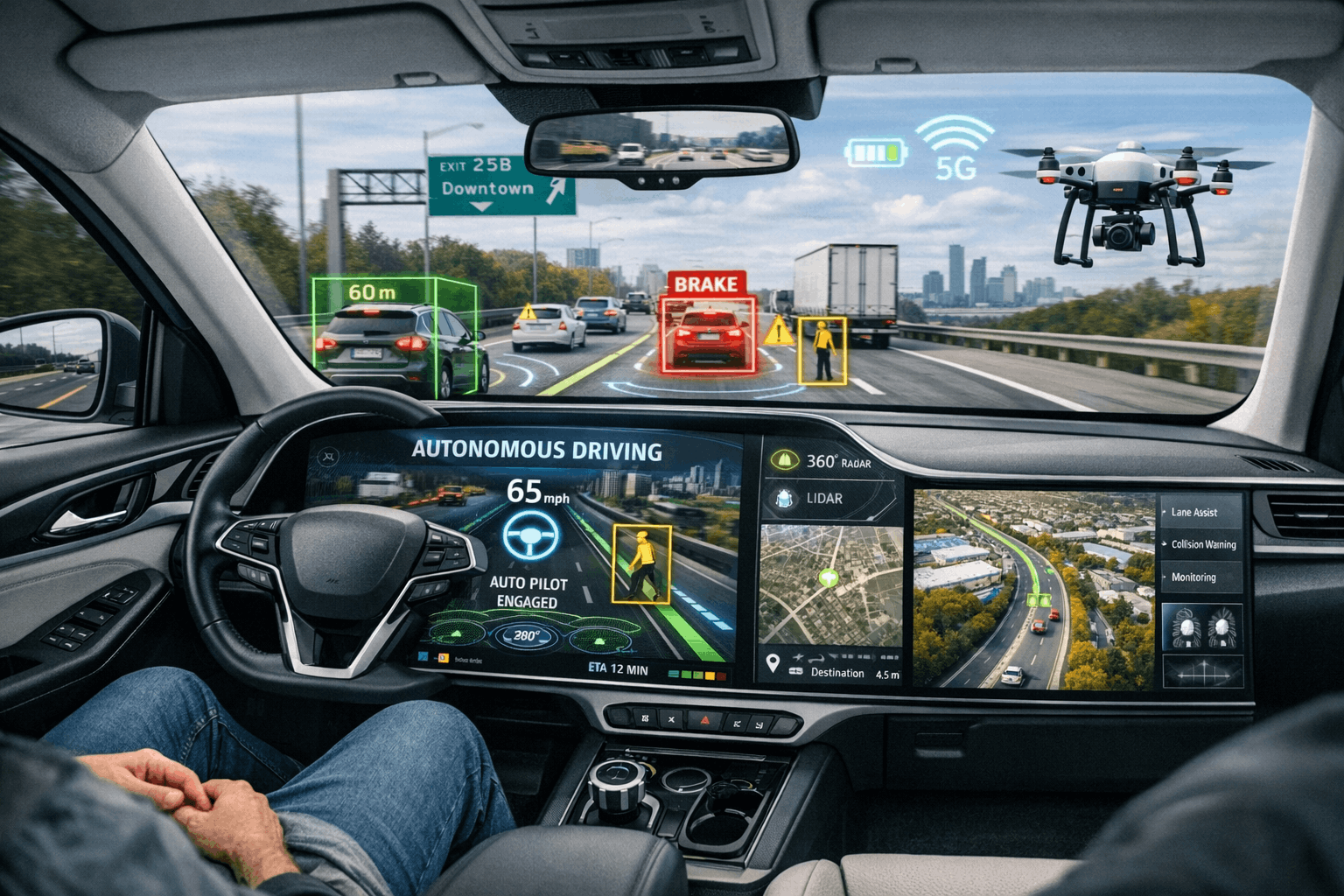

Autonomous driving technology uses AI-powered sensor fusion systems, HD mapping infrastructure, and sophisticated vehicle control software to enable vehicles to navigate complex road environments across five defined automation levels. The opportunities in this market exist at every level of the value chain from semiconductor and sensor manufacturing through AI software development, HD mapping services, vehicle integration, fleet operations, and the MaaS platforms that monetize autonomous driving capability through subscription and per-trip service models.

Understanding the full opportunity landscape requires engaging with both the hardware and software dimensions and the platform and service business models that are creating the most significant long-term value in a market where the economics of autonomous driving are shifting from capital-intensive development investment toward commercially scalable service delivery.

Market Segmentation: Level of Automation, Component and Application

By Level of Automation

The Level 2 automation opportunity is the most immediately accessible and the largest by volume across the global new vehicle production base, with every major automotive OEM and tier-one ADAS supplier competing for specification positions in programs that collectively represent tens of millions of vehicles annually. The Level 3 conditional automation opportunity is the most commercially activating near-term opportunity for OEMs with the engineering capability and regulatory approval infrastructure to offer legal Level 3 operation in major markets, where first-mover positioning in this emerging category creates premium pricing opportunities and customer loyalty advantages. The Level 4 high automation opportunity is the most transformative commercially, with the robo-taxi and autonomous commercial vehicle application categories offering Mobility-as-a-Service business models that can generate recurring per-mile revenue far exceeding the one-time economics of conventional vehicle sales.

By Component

The Hardware component opportunity is most compelling in the solid-state LiDAR and automotive-grade AI computing platform categories where technology cost reduction is creating expanding markets as previously unaffordable autonomous sensing systems reach the price points required for mainstream vehicle integration. The Software component opportunity is the most valuable long-term, where AI platform licensing, map data subscriptions, over-the-air update services, and safety monitoring platforms create recurring revenue streams that transform automotive business models from transactional hardware sales toward ongoing service relationships with far superior unit economics over vehicle lifetimes.

By Application

The Consumer application opportunity is the largest in total addressable market terms, encompassing the progressive ADAS adoption across the global vehicle fleet and the subsequent transition toward Level 3 and Level 4 personal vehicle autonomy that will unfold across the forecast period as technology capability and regulatory approval progressively expand the range of conditions under which autonomous operation is commercially available. The Ride Sharing application opportunity is generating the most commercially visible near-term autonomous driving revenue through robo-taxi services that are demonstrating the unit economics of driverless passenger transportation at commercial scale for the first time.

The Car Sharing application opportunity is developing as autonomous vehicles create the possibility of self-delivering vehicles that eliminate the repositioning labor cost that represents one of the most significant operational challenges in conventional car sharing programs. The Public Transit application opportunity is developing through autonomous bus and shuttle programs that can extend public transportation coverage to areas and times where human-driven service is economically unviable, creating new social infrastructure value alongside commercial opportunity.

Frequently Asked Questions

What are the biggest opportunities in the Autonomous Driving Market through 2031?

The biggest opportunities lie in AI software platform development that creates recurring revenue through vehicle subscriptions and OTA updates, Level 4 robo-taxi operations that enable Mobility-as-a-Service business models, geographic expansion into Asia-Pacific markets where autonomous vehicle investment is growing rapidly, and compliance-driven ADAS adoption that is embedding autonomous technology into mainstream vehicle production at an accelerating rate globally.

How is the Mobility-as-a-Service model creating opportunities in the Autonomous Driving Market?

Mobility-as-a-Service models enabled by autonomous driving create per-mile recurring revenue that is far more financially attractive than one-time vehicle sales economics, enabling robo-taxi and autonomous shuttle operators to generate continuous commercial returns from a single vehicle asset deployed across high daily utilization in urban transportation service without the driver labor cost that makes human-driven MaaS operationally challenging at scale.

Which geographic regions offer the most significant autonomous driving market opportunities through 2031?

North America offers the most commercially mature Level 4 deployment opportunity through robo-taxi expansion. Asia-Pacific offers the largest total volume opportunity given China's extraordinary autonomous vehicle investment scale and the region's vast new vehicle production base adopting ADAS features. Europe offers a focused regulatory-driven Level 3 adoption opportunity where the EU's clear regulatory framework is creating the most predictable pathway to conditional automation commercial deployment.

Regional Outlook

North America represents the most commercially advanced opportunity landscape for Level 4 robo-taxi and autonomous commercial vehicle applications. Asia-Pacific represents the largest absolute volume opportunity given the scale of Chinese autonomous vehicle investment and the region's dominant new vehicle production. Europe represents a focused Level 3 adoption opportunity backed by the EU's regulatory framework. The Middle East and Africa and South and Central America represent developing opportunities where smart city infrastructure investment and mobility service development are creating entry points for autonomous driving technology deployment ahead of personal vehicle market maturity.

Key Company Profiles

- Volvo Car Corporation

- Toyota Motor Corporation

- Tesla, Inc.

- NVIDIA Corporation

- Intel Corporation

- General Motors Company

- Ford Motor Company

- Daimler AG

- Continental AG

Conclusion

The autonomous driving market opportunities through 2031 are as real, as substantial, and as commercially transformative as any in the global technology landscape. In a market growing at 16.3% CAGR and redefining the fundamental economics and experience of human mobility, the opportunities for companies that engage with the specific technical requirements, commercial models, and regulatory dynamics of autonomous driving with genuine capability and strategic clarity are among the most consequential available to any participant in the automotive, technology, or mobility service sectors today.

About The Insight Partners

The Insight Partners is among the leading market research and consulting firms in the world. We take pride in delivering exclusive reports along with sophisticated strategic and tactical insights into the industry. Reports are generated through a combination of primary and secondary research, solely aimed at giving our clientele a knowledge-based insight into the market and domain. This is done to assist clients in making wiser business decisions. A holistic perspective in every study undertaken form an integral part of our research methodology and makes the report unique and reliable.

Contact Us

If you have any queries about this report or if you would like further information, please contact us:

Phone: +1-646-491-9876

E-mail: sales@theinsightpartners.com

Also Available In: Korean German Japanese French Chinese Italian Spanish